|

|||||||||

|

|

|||||||||

|

|||||||||

|

|

|||||||||

|

Executive Summary

Geopolitical uncertainty continues to drive energy price volatility, affecting growth, inflation, and sentiment. ECB raises rates by 25 bp, while Brazil and Russia focus on stimulus with 25 bp cuts.

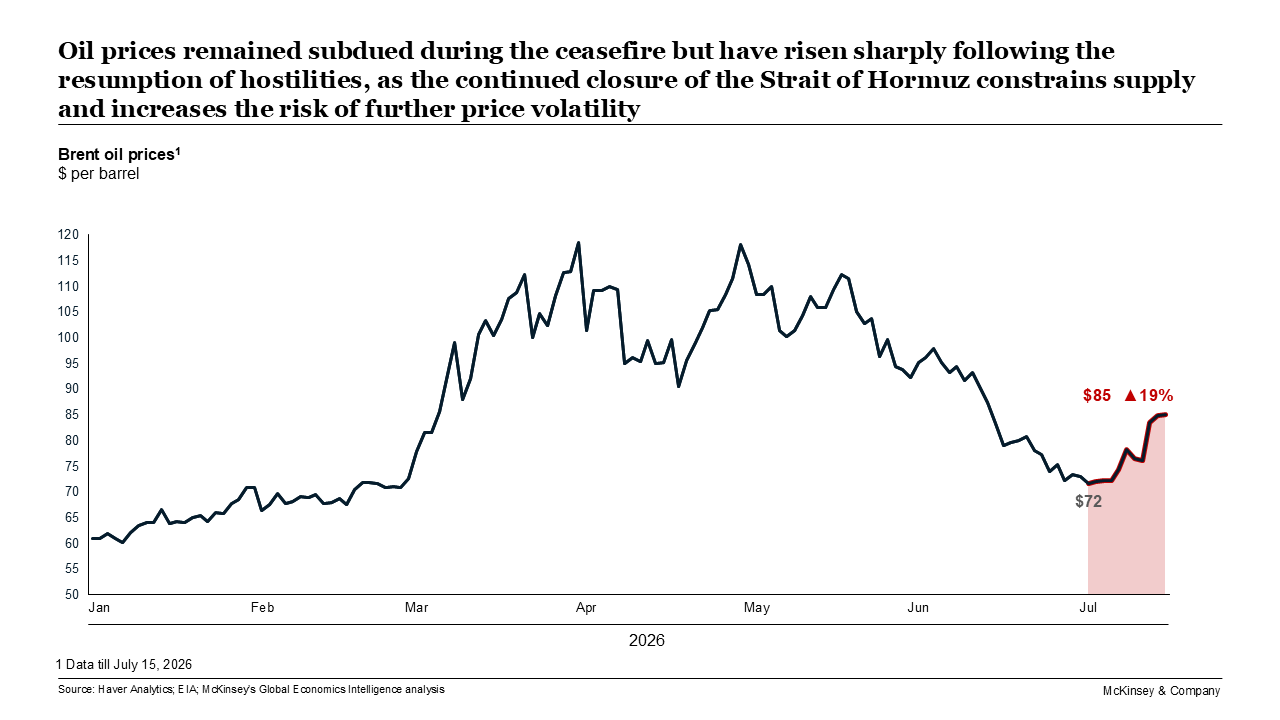

Recently, global attention has been focusing on two topics: the continuing uncertainty in the Persian Gulf and the outcome of the FIFA World Cup—both matters driving something of a roller-coaster of emotions among commentators, world leaders, and the public. Of the two issues, it will be the Gulf conflict that shapes global economic and, to some extent, political sentiment for the foreseeable future. In past weeks, the price of oil spiked and then retreated toward $75 a barrel; however, more recent events in the Gulf have injected a fresh geopolitical risk premium into energy markets. The wider global economy now awaits the next developments in the Middle East conflict as the combatants trade rhetoric and military strikes while talks continue in the background. Meanwhile, Europe’s gas and heating-oil bills remain stubbornly high and, more widely, food inflation is starting to creep back up, with real prices climbing around 5% for vegetable oils and meat (though this rise is still far below the 2022 shock). Among developed markets, inflation is drifting back to 2–4%, led by the United States where inflation reached 3.5% in June. The US consumer price index (CPI) increased 4.2% year over year in May, after rising 3.8% in April. Core inflation rose 2.9% (annualized). In May, median inflation expectations were down by 0.1 percentage points to 3.5% at the one-year-ahead horizon. Across most emerging economies inflation has ticked up. CPI in China reached 1.2% year over year in May, while core inflation stood at 1.1%. At the factory gate, however, producer prices rose 4.1% year on year, following a 3.9% increase in May. In India, retail inflation rose to 3.93% in May (up from 3.48% in April) on higher food prices, reaching a 16-month high and the steepest rise recorded under the new CPI series (base year 2024). Growth remains subdued in the face of geopolitical uncertainty, especially where energy prices are an issue. The euro area’s economy contracted by 0.2% quarter on quarter in Q1 2026—the first quarterly contraction since 2023—while growing only 0.3% year on year. The contraction reflects the cumulative drag from Middle East–driven energy prices, weakening external demand, and tighter financial conditions persisting across the bloc. Similarly, in the UK, recent data points to softer underlying activity following a relatively resilient Q1. Monthly real GDP fell by 0.1% in April, driven primarily by weaker services output. The Office for National Statistics (ONS) has noted that firms in manufacturing, wholesale, and travel have cited ongoing Middle East tensions as a drag on activity. |

|||||||||

|

|

|||||||||

|

|||||||||

|

|

|||||||||

|

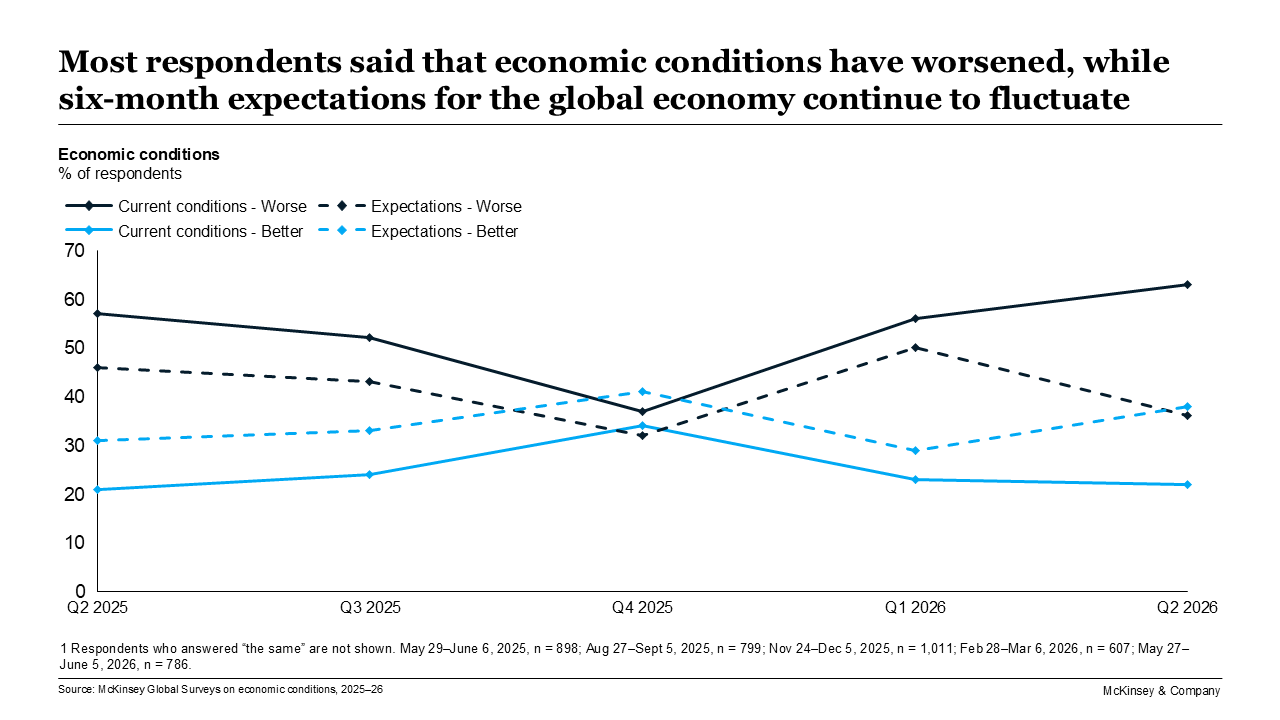

So, what is sentiment like on the ground? Early June saw executives more downbeat on the economy than they have been in years, according to the most recent

McKinsey Global Survey on economic conditions, which was conducted May 27 to June 5. “

Economic conditions outlook, June 2026” reported divided expectations for the coming months, with energy prices looming large in the minds of executives, alongside geopolitical instability. In this latest survey, a larger proportion of respondents also cited inflation and supply chain disruptions as top risks to the global economy.

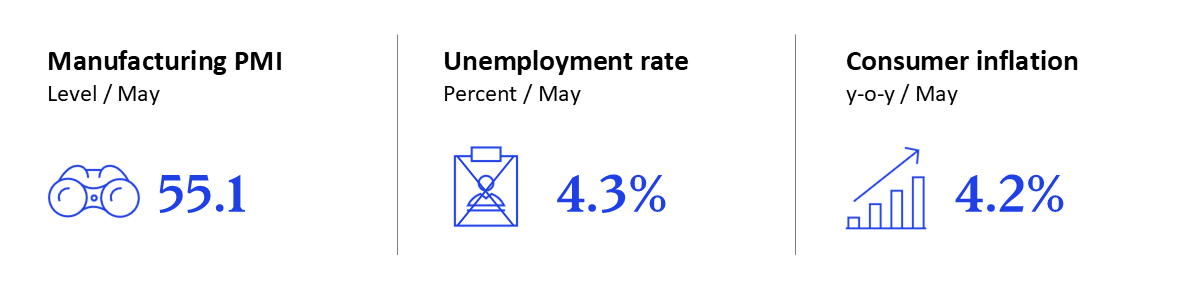

Nearly two-thirds of those surveyed said conditions in the global economy had worsened over the past six months (the largest share since June 2022), with a majority (54%) reporting worsening conditions in their national economies as well—notably, the largest share since respondents reflected on the COVID-19 pandemic’s early days in the September 2020 survey. That said, executives were less pessimistic about the global economy’s future than in the previous quarter. Respondents said their companies have been making defensive changes in response to external shocks. In terms of consumer confidence, households are largely staying on the sidelines, with confidence continuing to deteriorate and no clear rebound recorded across major economies. At the same time, consumers are dividing into two camps globally, as Brazil, Russia, and the United States keep on spending while China, the eurozone, and the UK stall. In the US, retail and food services sales in May (adjusted for seasonal variation and holiday and trading-day differences) reached $763.7 billion, up 0.9% from April’s revised $757.0 billion. Nevertheless, consumer sentiment in the eurozone is showing early signs of a fragile recovery. The European Commission’s flash consumer confidence index improved for a second consecutive month in June, rising to –17.7 from –19.0 in May and recovering from a multiyear low of –20.6 in April, suggesting that households may be beginning to adapt to persistently elevated energy costs. How are central banks reacting? The easing cycle has reached emerging markets first, with Brazil and Russia both making policy rate cuts—Russia and Brazil’s central banks both cut their key rates by 25 basis points to 14.25%—while the Federal Reserve and the Bank of England (BoE) kept rates on hold. By contrast, the European Central Bank (ECB) raised all three key interest rates by 25 basis points in June—the first rate hike since September 2023. Accordingly, the interest rates on the deposit facility, the main refinancing operations, and the marginal lending facility were increased to 2.25%, 2.40%, and 2.65% respectively, with effect from June 17. Looking ahead, we see that global growth is managing to maintain its footing with positive sentiment among executives reflected in both the global manufacturing (52.7) and services (52.0) purchasing managers’ indexes (PMIs), which are pointing to steady expansion. Factories in various economies continued to expand in May—notably in the US, UK, and India—while those in Brazil and Russia remained in the contraction zone. In the US, the industrial production index increased slightly to 102.6 in May, while S&P’s Manufacturing PMI climbed to 55.1 (54.5 in April). |

|||||||||

|

|

|||||||||

|

|||||||||

|

|

|||||||||

|

Services sentiment, meanwhile, is telling two stories: India and China are powering ahead, while the UK, Eurozone, and Russia remain stuck below 50. In the US, the services PMI eased to 50.7 in May (51.0 in April). India saw the services PMI slip to a 17-month low of 57.3 in June (from 59.8)—pulling the composite PMI to 57.4—its weakest level since March but still robustly in expansion territory.

Looking at employment, we see that US non-farm payroll employment rose by 172,000 in May. Job gains were recorded in leisure and hospitality, local government, and healthcare. Employment in financial activities declined. Unemployment remained at 4.3%. Overall, market volatility has been relatively modest despite the energy situation. VIX has remained relatively low, near 20 (within the historical average range), while oil price volatility spiked to multiyear highs in the face of the Gulf conflict before retreating. Equity markets have headed in both directions, according to local economic sentiment: Japan and the US reached new highs while Russia (–8% in June) and Brazil experienced a sell-off. In May, the S&P 500 was up 5.2%, bringing the one-year return to approximately 29.8%; the Dow Jones climbed 2.9% over the month and posted approximately a 22.7% one-year return. Similarly, government borrowing has seen bond markets diverge: Brazil’s 10-year rate topped 14% while China’s has been sinking toward 1.5%. Developed markets, meanwhile, anchored around 4%. Turning to trade, we see that global export momentum remained uneven in the first few months of 2026, with growth concentrated in the United States, China, and Mexico, while import demand diverged across major economies, with strong growth in China, India, and Mexico. Meanwhile, global shipping activity softened in April, pointing to weaker trade momentum as geopolitical disruptions have persisted. Global supply-chain pressures remained elevated in May, reaching the highest level since 2022. US-bound shipping rates from Shanghai rose modestly over April to May amid the renewed geopolitical disruptions; in the opposite direction, US-to-China freight rates rose in April but remained well below the elevated levels seen in 2025. In the US, April’s exports reached $327.1 billion, up $8.3 billion on the March figures. April imports hit $383.0 billion, $7.6 billion more than in March. The monthly deficit decreased by 1.2% to $55.9 billion. May saw China’s exports reach RMB 2.59 trillion (some $382 billion) with imports at RMB 1.86 trillion (approximately $275 billion), producing a trade surplus of roughly RMB 724 billion, equivalent to about $105 billion.

* * *

Global geopolitical shifts call for a new “cartography of competitiveness”—that’s the conclusion of a June 30 report from McKinsey Global Institute. In a debate often characterized by vague calls for “cutting red tape” or “structural reforms,” Catalyzing competitiveness: Where investment happens and why makes the case for using productive investment as a proxy for competitiveness and charts a detailed line-by-line map of what investments happen where and why. The research indicates that investment has stalled in Europe, shifted in the United States, and pulled away from the pack in China, with the divergence posing different challenges in each region. While Europe will need to close its €800 billion annual investment gap, the challenge for the US is to increase investment in manufacturing to reduce dependency on imports. Meanwhile, China is adding three times more productive assets each year than Europe and the US combined, yet capital returns are roughly 40 percent lower. Cost differentials, time to market, and productivity levels are all influencing the overall picture. Rebalancing investment requires a boost in productivity and innovation, specialization in less cost-sensitive industries, and policies to level the playing field. The authors conclude that restoring competitiveness where it is lacking will require real change from governments and companies on multiple fronts, and they make suggestions about potential ways forward. |

|||||||||

|

|

|||||||||

|

|||||||||

|

|||||||||

|

Regional and Country Summary

US CPI increased 4.2% year over year in May; eurozone trade balance swings to first monthly deficit in over a year; UK economy lost momentum entering Q2.

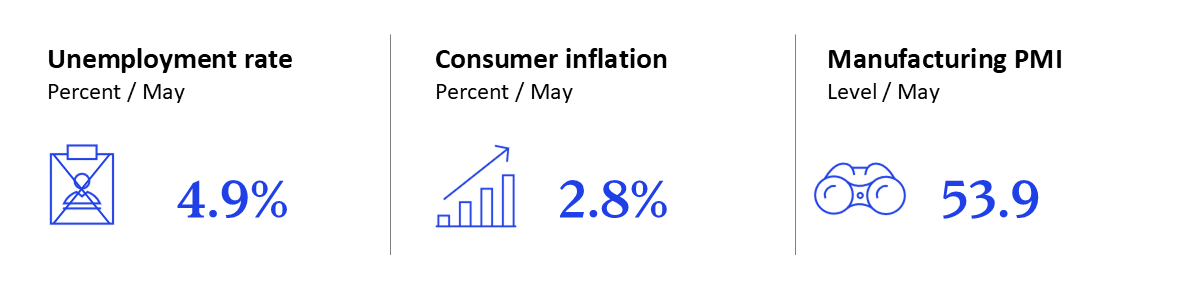

United States Inflation rises to 4.2% year over year; housing starts drop 15.4%; FIFA World Cup kicks off. The consumer price index (CPI) increased 4.2% year over year in May, after rising 3.8% in April. Core inflation rose 2.9% (annualized). In May, median inflation expectations were down by 0.1 percentage points to 3.5% at the one-year-ahead horizon. On the housing market, the 30-year fixed-rate mortgage increased slightly to 6.5% in May. Existing home sales increased by 3.2% in May, while housing residential starts declined to 1,177,000 (below the revised April estimate of 1,392,000)—a 15.4% drop and the lowest level since 2020. Completions in May were down 8.1%, reaching 1,313,000, compared with the revised April estimate of 1,429,000. Non-farm payroll employment rose by 172,000 in May. Job gains were recorded in leisure and hospitality, local government, and healthcare. Employment in financial activities declined. Unemployment remained at 4.3%. April exports reached $327.1 billion, up $8.3 billion on the March figures. April imports were $383.0 billion, $7.6 billion more than in March. The monthly deficit decreased by 1.2% to $55.9 billion. |

|||||||||

|

|

|||||||||

|

|||||||||

|

|

|||||||||

|

May’s retail and food services sales (adjusted for seasonal variation and holiday and trading-day differences) reached $763.7 billion, up 0.9% from April’s revised $757.0 billion.

The industrial production index increased slightly to 102.6 in May. S&P’s Manufacturing PMI climbed to 55.1 in May 2026 (54.5 in April); the services PMI eased to 50.7 in May (51.0 in April). In May, the S&P 500 was up 5.2%, bringing the one-year return to approximately 29.8%; the Dow Jones climbed 2.9% over the month and posted approximately a 22.7% one-year return. April’s CBOE Volatility Index was down to 15.3 (after dropping to 17 in April). The Federal Reserve maintained the federal funds rate at 3.50–3.75% at its June 16–17 meeting. The Board also kept the interest rate paid on reserve balances at 3.65%, effective June 18, leaving the operational stance of monetary policy broadly unchanged. The 2026 FIFA World Cup is underway across the United States, Canada, and Mexico, marking the first tournament hosted by three countries and the largest in World Cup history with 48 teams. FIFA expects roughly 6.5 million attendees over the course of the tournament, with matches being played in 16 host cities across North America. Ship traffic through the Strait of Hormuz has increased since the United States and Iran signed an interim memorandum of understanding to end hostilities and reopen the strategic waterway. While vessel volumes remain below prewar levels, commercial shipping has resumed and both countries are negotiating a longer-term framework. |

|||||||||

|

|

|||||||||

|

|

|||||||||

|

Eurozone

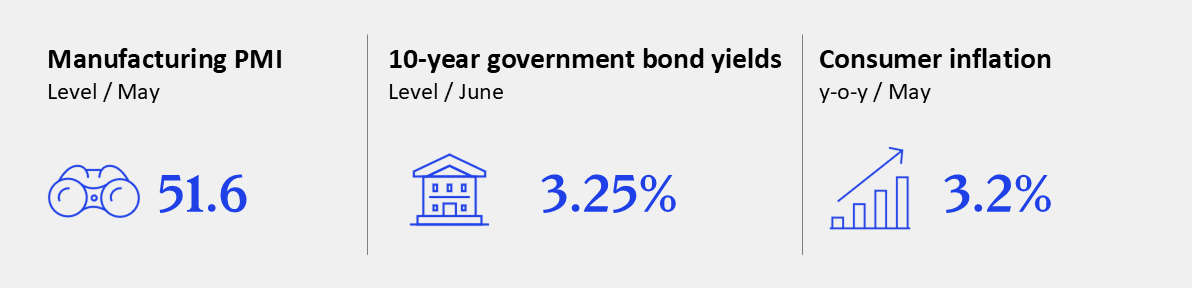

In the first quarter of 2026, eurozone GDP contracted 0.2% quarter on quarter; headline inflation reached 3.2%; trade balance swings to first monthly deficit in over a year. The euro area’s economy contracted by 0.2% quarter on quarter in Q1 2026—the first quarterly contraction since 2023—while growing only 0.3% year on year. This marks a sharp reversal from the 0.2% expansion recorded in Q4 2025 and broadly missed market expectations. The contraction reflects the cumulative drag from Middle East–driven energy prices, weakening external demand, and tighter financial conditions persisting across the bloc. Excluding Ireland, the eurozone economy grew by approximately 0.2% in Q1, broadly in line with Q4 2025. While the headline figure technically marks the first contraction since 2023, underlying activity across the rest of the bloc remains meaningfully more resilient than the top-line figure suggests. Headline HICP (Harmonized Index of Consumer Prices) inflation accelerated to 3.2% year on year in May 2026, up from 3.0% in April and 2.6% in March. The increase was primarily driven by energy prices, which surged by more than 10% year on year. Persistence of the Middle East conflict and disruptions in the Strait of Hormuz are keeping energy costs structurally elevated. Core inflation held at approximately 2.2% in April, remaining above the European Central Bank’s (ECB) 2% target. |

|||||||||

|

|

|||||||||

|

|||||||||

|

|

|||||||||

|

Consumer sentiment is showing early signs of recovery. The European Commission’s flash consumer confidence index improved for a second consecutive month in June, rising to –17.7 from –19.0 in May and recovering from a multiyear low of –20.6 in April, suggesting that households may be beginning to adapt to persistently elevated energy costs. The recovery remains fragile: retail sales fell 0.4% month on month in April, and confidence continues well below its long-term average. Energy relief measures introduced by several eurozone governments may be starting to provide modest support.

Incoming data suggest that the downturn in business activity is gradually easing. Industrial production edged up by 0.1% month on month in April 2026. The S&P Global Flash Eurozone Composite Purchasing Managers’ Index (PMI) rose to 49.5 in June 2026 (a three-month high, up from 48.5 in May), signaling near-stabilization in private sector output. Manufacturing output returned to expansion at 51.2, while services activity contracted modestly to 48.9. Supply chain delays remain widespread and inflationary pressures, although easing, are still elevated. On June 11, the ECB Governing Council raised all three key interest rates by 25 basis points—its first rate hike since September 2023, following eight consecutive rate cuts implemented during 2024–25. Driven by persistent energy-price inflation linked to the Middle East conflict and disruptions in the Strait of Hormuz, the deposit facility rate increased to 2.25%. New Eurosystem staff projections foresee inflation averaging 3.0% in 2026 and GDP growth of 0.8%, a downward revision that underscores the severity of the energy shock on real incomes and consumer confidence. |

|||||||||

|

|

|||||||||

|

|

|||||||||

|

United Kingdom

UK economy lost momentum entering Q2, with weaker activity indicators reinforcing expectations of modest growth, while political uncertainty increased. Recent data pointed to softer underlying activity following a relatively resilient Q1. Monthly real GDP fell by 0.1% in April, driven primarily by weaker services output, while Bank of England staff judged that the reported 0.6% expansion in Q1 likely overstated underlying momentum—they estimate underlying quarterly growth at around 0.2% in both Q1 and Q2. That suggests activity entered Q2 on a weaker footing than the headline GDP figures initially implied. The Office for National Statistics (ONS) also noted that firms in manufacturing, wholesale, and travel cited ongoing Middle East tensions as a drag on activity. Household spending provided some temporary support. Retail sales volumes rose 1.2% in May, while non-store retailer sales volumes increased 6.1%. However, the ONS pointed to unusually hot weather and promotions as important drivers rather than a durable demand recovery. Consistent with that, the GfK consumer confidence index held at –23 in June, suggesting households remain cautious despite the stronger retail print. Labor market indicators continued to point to softer labor demand with vacancies falling to 707,000—their lowest level since 2021—and payrolled employment remaining weak, even as unemployment edged down to 4.9%. Together, these trends suggest that household demand is likely to remain fragile and uneven over coming quarters. Inflation developments were mixed. Headline consumer price inflation (CPI) remained unchanged at 2.8% in May. Services inflation rose to 3.7% from 3.2% in April, while core CPI edged up to 2.6% from 2.5%. Together, these point to some persistence in underlying inflation pressures, although part of May’s increase reflected transport, travel, and energy-related components. However, lower food-price inflation and softer goods inflation helped offset these increases to leave the headline rate unchanged. |

|||||||||

|

|

|||||||||

|

|||||||||

|

|

|||||||||

|

The latest Monetary Policy Committee (MPC) decision on 18 June held the Bank Rate at 3.75% by a 7–2 vote. The increase from one to two votes in favor of a rate rise suggests that some policymakers remain concerned about the persistence of inflation, even as the committee acknowledged weaker activity and a loosening labor market. MPC also noted that household one-year inflation expectations had risen from 3.2% in February to 4.0% in May—the highest reading since February 2023—highlighting concerns that higher energy costs could continue to feed through into broader price and wage-setting behavior.

Fiscal conditions also remained tight. Government borrowing reached £23.3 billion last month, the second-highest May borrowing figure on record and above the Office for Budget Responsibility’s forecast. Debt interest payments hit £11.7 billion for the month while public debt rose to 95.1% of GDP, adding to pressure on fiscal headroom should growth weaken further. Growing spending demands—including defense—are placing additional pressure on an already constrained fiscal position. Financial markets remained sensitive to these pressures: although gilt yields retreated from the highs reached in May, the 10-year yield stayed close to 4.8% in June. Externally, the OECD’s June Economic Outlook projected UK GDP growth of 0.9% in 2026 and 1.1% in 2027, consistent with a prolonged period of below-trend growth. On 22 June, Prime Minister Keir Starmer announced his intention to resign. His successor, now known to be Andy Burnham, will become the UK’s seventh prime minister in a decade, extending a period of elevated political turnover and adding another layer of uncertainty to the policy environment. |

|||||||||

|

|

|||||||||

|

|

|||||||||

|

China economy heading down two tracks; India’s economy stabilizing as oil prices ease; Brazil and Russia cut rates.

China

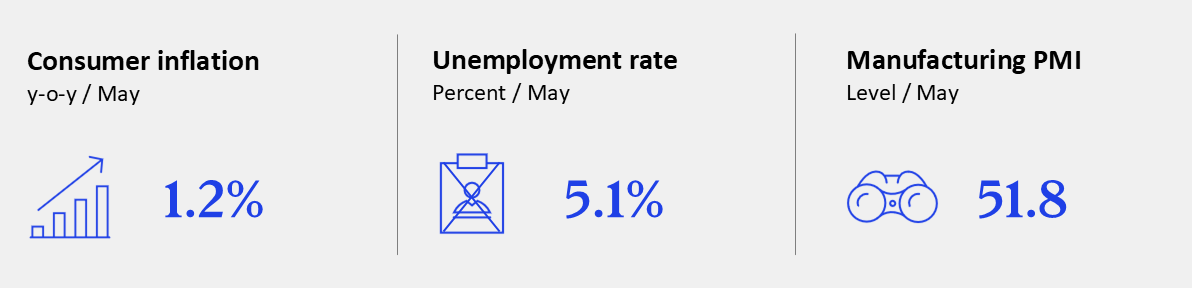

China’s expansion is increasingly running along two tracks: an external and industrial engine that is firming, set against a domestic demand base which remains weak—this divergence leaves the central bank maintaining an accommodative stance while keeping benchmark lending rates unchanged. Looking at China’s industrial performance, the monthly data point to some loss of momentum: industrial value added was up 4.5% year over year in May, while the manufacturing purchasing managers’ index (PMI) rose to 50.3 in June from 50.0 in May—indicating somewhat fragile recovery rather than a strong rebound. Consumer price inflation (CPI) reached 1.2% year over year in May, while core inflation stood at 1.1%. At the factory gate, however, producer prices rose 4.1% year on year, following a 3.9% increase in May. The household side of the economy continues to be the clearest source of weakness. Retail sales fell 0.6% year over year in May, although they were still up 1.4% over the first five months of the year. The urban surveyed unemployment rate eased to 5.1% in May from 5.2% in April, but the broader employment picture remains soft. Housing is also still in contraction: new-home prices across 70 cities fell 3.5% year over year and 0.2% month over month in May. Together, weak consumption and continued declines in property prices suggest that household confidence and domestic demand have yet to turn decisively. |

|||||||||

|

|

|||||||||

|

|||||||||

|

|

|||||||||

|

The external sector, by contrast, remains a major source of support. In May, exports reached RMB 2.59 trillion and imports RMB 1.86 trillion, producing a trade surplus of roughly RMB 724 billion, equivalent to about $105 billion.

The People’s Bank of China (PBOC) has kept benchmark lending rates unchanged. The one-year loan prime rate remains at 3.0%, while the over-five-year rate—most relevant for mortgage pricing—stands at 3.5%. The central bank continues to emphasize liquidity support and structural policy tools while maintaining an accommodative stance overall. |

|||||||||

|

|

|||||||||

|

|

|||||||||

|

India

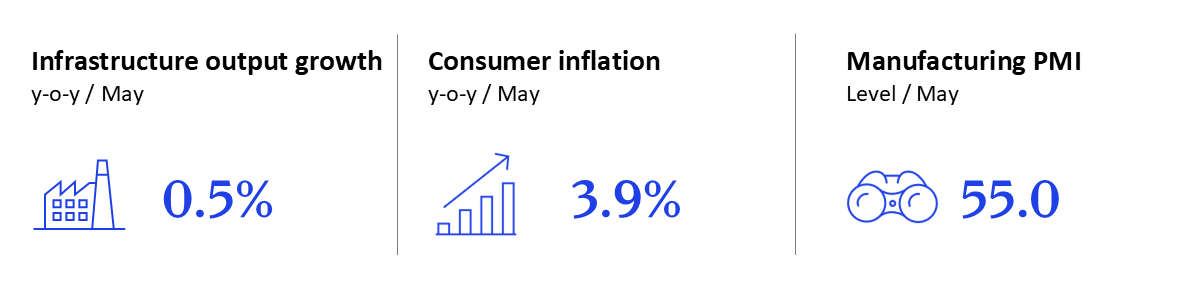

Economy stabilizing as oil prices ease; RBI trims FY 2026–27 projection to 6.6%; CPI rises. India’s economy is stabilizing as the US-Iran interim peace agreement eases the West Asia supply shock, pulling the Brent crude price below $80—down from above $100 in May. National Statistical Office (NSO) data (June 5) put FY 2025–26 real GDP growth at 7.7%, while the Reserve Bank of India’s (RBI) June 5 review trimmed its FY 2026–27 projection to 6.6% from 6.9%. This reflects the lingering drag from earlier energy disruptions and global financial volatility. The HSBC Flash India Manufacturing Purchasing Managers’ Index (PMI) eased to 54.5 in June from 55.0, a three-month low, as demand and hiring softened, while services slipped to a 17-month low of 57.3 from 59.8, pulling the composite PMI to 57.4—its weakest since March but still firmly in expansion. Infrastructure (core sector) output grew just 0.5% year on year in May, a seven-month low (April revised up to 1.8%), led by electricity, cement, and steel, up 8.7%, 8.4%, and 5.0% respectively. Meanwhile, coal fell 9.3%, crude oil 4.6%, natural gas 4.9%, refinery products 8.7%, and fertilizers 0.9%. With the Strait of Hormuz reopening after the ceasefire, supply-side pressure on the core sectors (40% of industrial production) should ease. |

|||||||||

|

|

|||||||||

|

|||||||||

|

|

|||||||||

|

Retail inflation rose to 3.93% in May, a 16-month high and the steepest under the new consumer price index (CPI) series (base year 2024), up from 3.48% in April, on higher food prices. Food inflation firmed to 4.78% from 4.20%, while core inflation rose for a third straight month to about 3.7%. This keeps inflation within RBI’s 2–6% band but just below its 4% medium-term target.

RBI raised its FY 2026–27 CPI forecast to 5.1% from 4.6%, citing the pass-through of higher energy costs. Equity markets recovered about 2% month to date in June, with the SENSEX near 76,300 as the ceasefire and falling crude prices eased risk sentiment. The rupee recovered to around 94.7 per dollar, from beyond 95 in May, aided by the ceasefire and RBI measures to attract currency inflows. Forex reserves stood at $671.6 billion as of June 12, down $9.99 billion on the week as lower gold prices cut the value of gold holdings, even as foreign currency assets rose. The merchandise trade deficit held steady month on month at $28.21 billion in May, based on $73.41 billion in imports and a record $45.20 billion in exports (up 18% year on year), though it widened from a year earlier given the higher oil and gold imports bill. Adopting a neutral stance, RBI held the repo rate at 5.25% with a unanimous vote at its June 5 review, but flagged inflation risks from energy prices and a sub-normal monsoon. With the conflict de-escalating, markets have pared rate-hike expectations, though RBI remains data-dependent and vigilant on second-order effects. India and the EU continued finalizing their comprehensive free trade agreement, with European Commission President Ursula von der Leyen confirming on June 17 it would be signed by the end of 2026 and coming into force in 2027. India and the US entered the final stages of an interim trade agreement, with US trade representative Jamieson Greer due in New Delhi on June 23–24 to finalize the framework ahead of July 24’s expiry date for temporary US tariffs. |

|||||||||

|

|

|||||||||

|

|

|||||||||

|

Brazil

Brazil´s central bank makes further policy rate cut despite worsening inflation. In a unanimous decision on June 17, Banco Central do Brazil’s Monetary Policy Committee (Copom) decided to cut the Selic rate by 25 basis points, to 14.25%. Copom noted for the first time the “need for smoothing economic activity levels and promoting full employment.” Various factors, however, including the war in the Middle East, are noted as reasons to be cautious for emerging economies such as Brazil. Inflation was up in April, touching 4.72% (against 4.39% in March), and above the central bank’s upper target limit of 4.50%. In response to rising energy costs, the government unveiled a new subsidy of BRL 0.44 per liter for gasoline producers and importers, starting May 25. Initially planned to run for two months, the subsidy will cost BRL 2.4 billion (approximately $461 million), which the government plans to recover through revenue driven by higher oil prices. The three-month moving average unemployment rate edged down towards 5.8% in April, compared with March’s 6.1%. On the financial markets, the average monthly real–dollar exchange rate was BRL 4.98 per USD in May (BRL 5.03 in April). The Bovespa equities index trended down in May, sliding 7.2%; performance has recently been declining with the index down 3.1% as of June 19. |

|||||||||

|

|

|||||||||

|

|||||||||

|

|

|||||||||

|

Consumer confidence stayed below the neutral 100 mark, with FGV’s seasonally adjusted April reading moving down to 88.8. Meanwhile, business confidence was unchanged at 90.9. Construction confidence was also steady at 92.6.

Brazil’s manufacturing production decreased: the Monthly Industrial Physical Production (PIM) Index slid from 104.1 in March to 101.9 in April (above the neutral 100 line). Factory production decreased 3.2%, while extractive production increased 2.6%. On aggregate, however, April 2026’s results were only 2.7% above those from the same period last year. The Monthly Services Survey (PMS) revenue index decreased to 127.9 in April from 130.7 in March (above the neutral 100 mark). This was mirrored in the volume index, which slid to 107.1 (from 109.5). The largest revenue decrease was in audiovisual services (down 12.4% since March), followed by other family services (down 6.3%). Meanwhile, audiovisual services’ volumes were down 12.2%, while the other land transportation segment decreased 6.5%. May’s trade balance recorded a surplus of $7.8 billion, down from $10.5 billion in April. The smaller surplus was the result of a larger decrease in exports ($31.9 billion in May, down from $34.2 billion in April) and an increase in imports ($24.1 billion in May, up from $23.6 billion in April). Brazilian Senator Flavio Bolsonaro, a potential candidate in October’s presidential election, has registered to testify at a July 6 trade hearing in the United States where he will oppose proposals for a 25% tariff on Brazilian goods. The tariffs stem from a US investigation into Brazil’s trade practices. Bolsonaro, who recently met President Donald Trump, said he is against the tariff, citing a desire to protect consumers, producers, and the longstanding United States–Brazil partnership. |

|||||||||

|

|

|||||||||

|

|

|||||||||

|

Russia

Russia entered mid-2026 with growth effectively stalled—but without a broad collapse in domestic demand; despite this slowdown, unemployment is still near a record low, while retail spending remains strong.

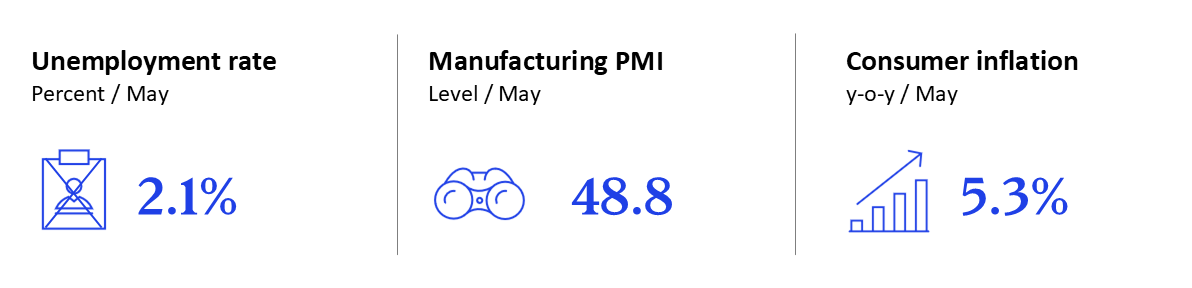

Industrial production fell 0.7% year over year in May after growing 1.9% in April. There are tentative signs of stabilization in manufacturing, where the purchasing managers’ index (PMI) rose to 50.3 in June from 48.8. However, the broader private-sector picture remains weak, with the services PMI falling further to 48.2 in June. Inflation is now complicating the monetary policy outlook. Headline consumer price inflation (CPI) slowed to 5.3% year over year in May (from 5.6% in April), helping to create room for the Central Bank of Russia (CBR) to continue easing monetary policy. That improvement, however, proved fragile: inflation reaccelerated to 6.0% in June. Producer prices had already pointed to renewed cost pressure, rising around 9.4% year over year in May after 5.5% in April. Unemployment fell to 2.1% in May—close to record lows—as demographic constraints, military mobilization, and ongoing demand from defense-related industries keep labor exceptionally scarce. That tight labor market continues to support household spending: retail sales rose 7.8% year over year in May, up from 6.5% in April. However, confidence remains weak. |

|||||||||

|

|

|||||||||

|

|||||||||

|

|

|||||||||

|

The central bank has continued to unwind some of its earlier monetary tightening, but cautiously. In June, CBR cut the key rate by 25 basis points to 14.25%. It emphasized that underlying inflation had moderated and that growth had weakened, but it also warned that fiscal policy was becoming more accommodative.

The external sector remains one of the economy’s stronger buffers. Russia recorded an $11.4 billion trade surplus in April, with exports of $38.8 billion exceeding imports of $27.4 billion, while the current account surplus reached $6.7 billion. The fiscal position, meanwhile, is becoming a more significant constraint—rather than a source of comfort. The federal budget deficit reached 2.6% of GDP in the first five months of 2026, already above the government’s 1.6% full-year target. The government has acknowledged that the full-year deficit is likely to exceed plan, while the central bank has warned that persistent structural primary deficits could require tighter monetary policy than previously assumed. Fiscal support may therefore cushion activity in the near term, but it also risks keeping inflation and interest rates higher for longer. |

|||||||||

|

|

|||||||||

|

|

|||||||||

|

Mexico

Mexico’s outlook remains mixed as inflation eases, labor markets stay resilient, peso holds firm, and trade surplus continues, while manufacturing picture improves slightly. The Bank of Mexico maintained the policy rate at 6.5% in June for a second month in a row. Meanwhile, annual inflation eased to 3.9% in May from 4.5% in April, marking a second consecutive decrease. Services inflation and non-core food prices remain the stickiest components. The peso appreciated marginally to MXN 17.3 per USD in May, from MXN 17.4 in April. Conditions in Mexico’s manufacturing sector improved slightly in May 2026 with the purchasing managers’ index (PMI) rising to 49.6 from April’s 47.7. A recovery in domestic new orders helped support sales and moderate the decline in production, but firms continue to face challenges from high costs, weak investment, tariffs, geopolitical tensions, and cash-flow constraints. Mexico’s labor market remained relatively strong, with the unemployment rate falling to 2.6% in April, from 2.8% in March. Formal employment totaled 22.7 million workers in May, though payrolls declined by 29,922 jobs (–0.1% month on month) due to seasonal agricultural effects and the removal of a fraudulent employer registration. Despite the monthly decline, employment continued to grow on an annual basis (+1.5% year over year), supported by gains in transportation, construction, social services, and manufacturing. |

|||||||||

|

|

|||||||||

|

|||||||||

|

|

|||||||||

|

Mexico’s trade surplus narrowed to $4.5 billion in April from $5.9 billion in March, as imports grew faster than exports even while both reached record levels. Exports rose to $72.0 billion ($70.7 billion in March), with manufacturing, which accounts for roughly 91% of the export base, expanding 34.0% year on year. Non-automotive manufactured goods such as electronics, medical devices, and appliances surged 45.8%, while automotive added a more modest 8.2%. Imports climbed to $67.5 billion (from $64.8 billion), driven by a 29.8% jump in intermediate goods, including raw materials and components feeding Mexican factories, which alone made up 80.3% of the import bill; capital goods rose just 1.3% and fuel imports fell 5.3%.

Mexico will host 13 matches during the 2026 World Cup. The opening match was played at the iconic Estadio Azteca in Mexico City, setting a new record with the stadium chosen as the venue for the World Cup opening ceremony for an unprecedented third time. The tournament is expected to generate between $2.3 billion and $4.0 billion in economic activity through visitor spending, temporary employment, and infrastructure improvements. Mexico City leads World Cup–related investments with more than $1.3 billion allocated to transportation, public space upgrades, mobility projects, and stadium modernization. Total World Cup–related investment could reach approximately $3 billion in Mexico. The opening weekend alone generated a $70 million economic boost for Mexico City, with local restaurants and bars reporting up to 40% increases in sales. |

|||||||||

|

|

|||||||||

|

|||||||||

|

|

|||||||||

|

|||||||||

|

McKinsey’s Global Economics Intelligence (GEI) provides macroeconomic data and analysis of the world economy. Each monthly release includes an executive summary on global critical trends and risks, as well as focused insights on the latest national and regional developments. Detailed visualized data for the global economy, with focused reports on selected individual economies, are also provided as PDF downloads on McKinsey.com. The reports available free to email subscribers and through the

McKinsey Insights App. To add a name to our subscriber list,

click here. GEI is a joint project of

McKinsey’s Strategy and Corporate Finance Practice and the

McKinsey Global Institute.

Shubham Singhal is the Chair of McKinsey's Global Institute and a senior partner in the Detroit office; Arvind Govindarajan is a partner in the Boston office. The data and analysis in McKinsey’s Global Economics Intelligence are developed by Jeffrey Condon, a senior expert in McKinsey’s Atlanta office; Krzysztof Kwiatkowski is an expert in the Boston office. The authors wish to thank Nick de Cent, as well as Masud Ally, José Álvares, Roman Büschgens, Darien Ghersinich, Gabriel Marini, Tomasz Mataczynski, Frances Matamoros, Alejandro Morales, Beatriz Oliveira, Debdoot Ray, Vanshika Tandon, Valeria Valverde, and Sebastian Vargas for their contributions to this article. |

|||||||||

|

|||||||||

|

The invasion of Ukraine continues to have deep human, as well as social and economic, impact across countries and sectors. The implications of the invasion are rapidly evolving and are inherently uncertain. As a result, this document, and the data and analysis it sets out, should be treated as a best-efforts perspective at a specific point of time, which seeks to help inform discussion and decisions taken by leaders of relevant organizations. The document does not set out economic or geopolitical forecasts and should not be treated as doing so. It also does not provide legal analysis, including but not limited to legal advice on sanctions or export control issues.

|

|||||||||

|

|

|||||||||

|